Key Takeaways

- China remains central to fiber, fabric, trims, machinery and scale manufacturing, so China+1 does not mean China exit.

- Vietnam and Bangladesh are strong garment platforms, but both need stronger fabric and yarn backward linkages.

- Indonesia and Cambodia benefit from diversification, but productivity, compliance, logistics and fabric access remain constraints.

- Sourcing teams are increasingly evaluating Asia by resilience, compliance data, lead time, material availability and product specialization, not only FOB cost.

- Exporters that can offer traceability, certified fabrics and reliable production planning will gain more than suppliers competing only on price.

Why This Insight Matters

China+1 sourcing has moved from a procurement slogan to a supplier qualification exercise. Global buyers still need China's scale and upstream strength, but they are also asking where risk can be reduced without weakening cost, quality or speed. For Asian textile companies, the real question is not whether orders will move. It is which orders move, which countries can absorb them, and which suppliers can prove reliability beyond low pricing.

Current Market Context

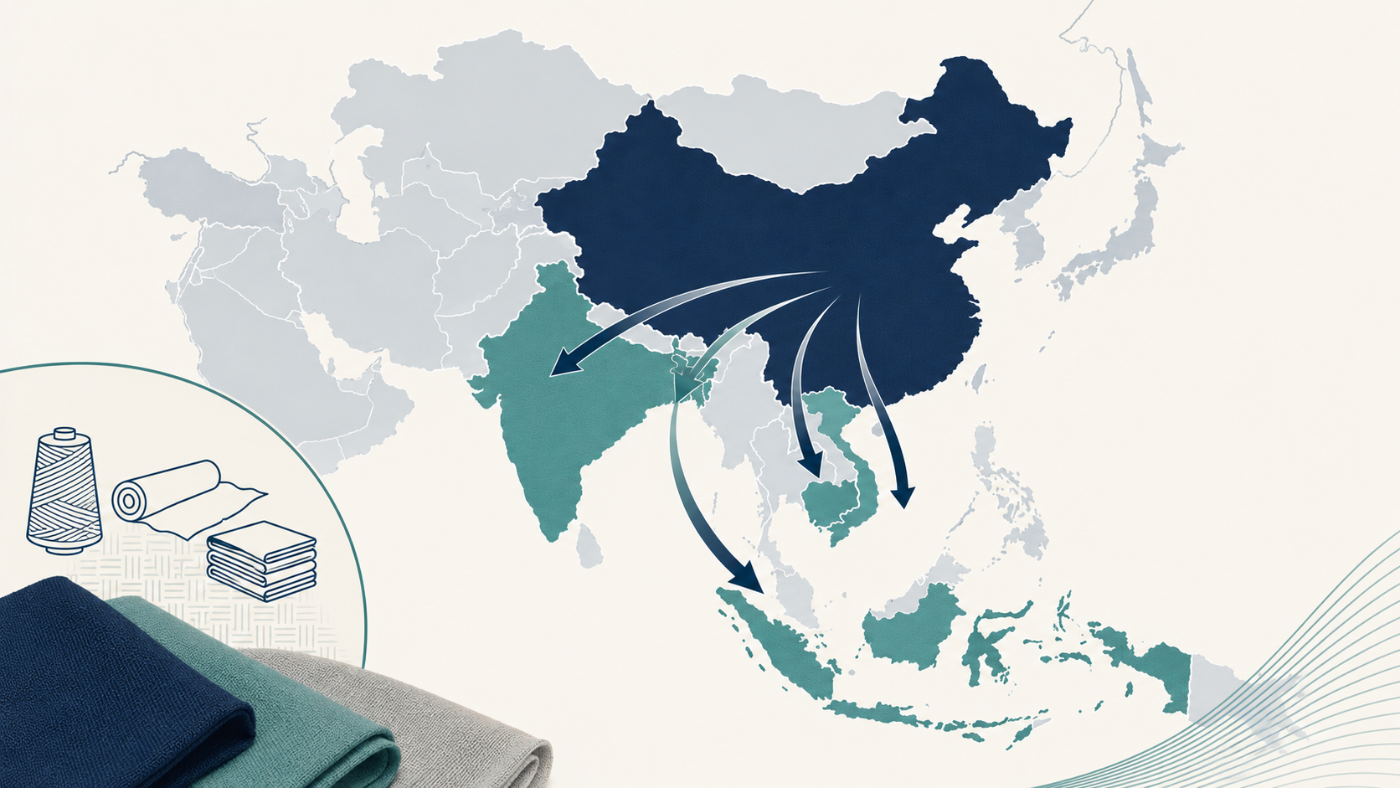

Across Asia, the sourcing map is becoming more segmented. China remains a leader in synthetic fibers, fabric development, trims, machinery, finishing know-how and speed. Vietnam is attractive for export manufacturing and trade access, but its dependence on imported fabric limits full supply-chain control. Bangladesh continues to hold scale in garment exports, especially cotton apparel, while pushing toward higher-value items and better waste use. India is trying to position itself as a broader textile platform with cotton, MMF, technical textiles, large parks and policy support. Indonesia offers a mix of labor, domestic textile capacity and regional access, while Cambodia remains important for labor-intensive garment production. WTO trade data shows that world goods and services trade rebounded in 2025, but the pattern is uneven and supplier resilience remains a board-level issue rather than a procurement footnote.

What Is Driving This Shift?

Risk diversification

Pandemic disruption, shipping volatility, geopolitical uncertainty and tariff exposure have made single-country dependence less acceptable. Brands increasingly want parallel capacity across Asia.

Fabric and material availability

Moving garment assembly is easier than moving yarn, fabric, dyeing, finishing, trims and testing. Countries with stronger backward integration are more likely to capture durable sourcing shifts.

Compliance and traceability

Supplier choice is being influenced by audit history, environmental data, wastewater controls, restricted substances management, and documentation quality.

Product specialization

Basic orders may move first, but long-term value will depend on performance fabrics, synthetic blends, recycled materials, outerwear, activewear, workwear and technical applications.

Country-Level View Across Asia

Country

Current Position

Opportunity

Key Challenge

China

Still the deepest textile ecosystem across fiber, fabric, dyeing, machinery and scale

Retain higher-value materials, innovation, speed and regional supply of inputs

Geopolitical risk, rising costs, buyer diversification

Vietnam

Strong export manufacturing and trade agreement positioning

Capture apparel orders from buyers seeking China+1 capacity

High dependence on imported fabric and inputs

Bangladesh

Major garment export hub with large workforce and buyer familiarity

Move from basic garments to value-added, recycled and synthetic categories

Energy, wage, compliance and backward linkage constraints

India

Broad raw material base, domestic market, policy push and integrated park ambition

Offer end-to-end textile and technical textile capacity

Fragmented supply chain and uneven processing quality

Indonesia

Established textile and apparel base with regional scale

Benefit from diversified apparel and fabric sourcing

Competition, logistics and modernization needs

Cambodia

Important labor-intensive garment supplier

Attract cost-sensitive diversification orders

Limited upstream textile base and compliance investment needs

Business Implications for Textile Companies

- Mills should develop certified fabric programs instead of waiting for garment exporters to pull demand.

- Garment exporters need dual strategies: maintain price competitiveness while adding design, fabric sourcing and compliance depth.

- Brands should map Tier-2 fabric and dyeing exposure, not only Tier-1 garment factories.

- Machinery suppliers can target modernization gaps in Vietnam, Bangladesh, India and Indonesia.

- Investors should look for integrated suppliers that combine material access, processing, compliance systems and export relationships.

Risks and Challenges

- China+1 can increase complexity if suppliers are added without fabric, trim and testing reliability.

- Newer sourcing destinations may face capacity bottlenecks during demand spikes.

- Compliance standards can expose documentation gaps across Tier-2 and Tier-3 suppliers.

- Lower labor cost does not automatically offset lower productivity or longer lead times.

- Dependence on imported yarn and fabric can reduce local value capture.

Opportunities to Watch

- Integrated textile parks and near-port manufacturing clusters

- Certified fabric platforms for global buyers

- Synthetic and performance fabrics for activewear and workwear

- Regional yarn-fabric-garment partnerships

- Digital supplier scorecards and traceability systems

Practical Recommendations

Map product categories by sourcing risk rather than shifting all orders together.

Build relationships with fabric mills in target countries before moving garment production.

Create buyer-ready documentation for origin, fiber content, dyeing, chemicals and testing.

Track trade policy, wage changes and energy costs by country each quarter.

Use pilot orders to test quality, lead time and compliance before scaling.

Invest in production planning and digital quality control to reduce buyer risk.

Develop China+1 strategies by product type: cotton basics, synthetic activewear, denim, outerwear, home textiles and technical fabrics.

Future Outlook

Over the next two to four years, China will remain deeply embedded in Asia's textile supply chain, but order allocation will continue to diversify. The strongest beneficiaries will be countries and suppliers that can combine competitive manufacturing with reliable fabric access, compliance documentation and predictable delivery. The next phase of China+1 will be less about geography and more about supplier capability.

Suggested Internal Links

- Technical Textiles in Asia: Applications and Growth Drivers

- Textile Recycling Technologies Explained

- Digital Product Passports in Textiles

- Sustainable Fabric Manufacturing Guide

- Textile Machinery Automation Trends

- Recycled Polyester vs Bio-Based Fibers

FAQs

Does China+1 mean textile buyers are leaving China?

No. Most buyers are reducing overdependence, not abandoning China. China remains important for fibers, fabrics, trims, machinery and speed.

Which Asian countries benefit most from China+1 textile sourcing?

Vietnam, Bangladesh, India, Indonesia and Cambodia are the most visible beneficiaries, but each has different strengths and bottlenecks.

Why is fabric availability important in China+1 sourcing?

Garment production depends on yarn, fabric, dyeing, finishing, trims and testing. If these are imported, lead time and risk remain high.

How can Indian textile suppliers benefit?

Indian suppliers can benefit by offering integrated fabric, processing, compliance and value-added categories such as MMF, technical textiles and home textiles.

What should brands check before shifting orders?

Brands should check production capacity, Tier-2 fabric sources, compliance records, lead times, testing facilities, waste handling and financial stability.